Oops…Ethics?!

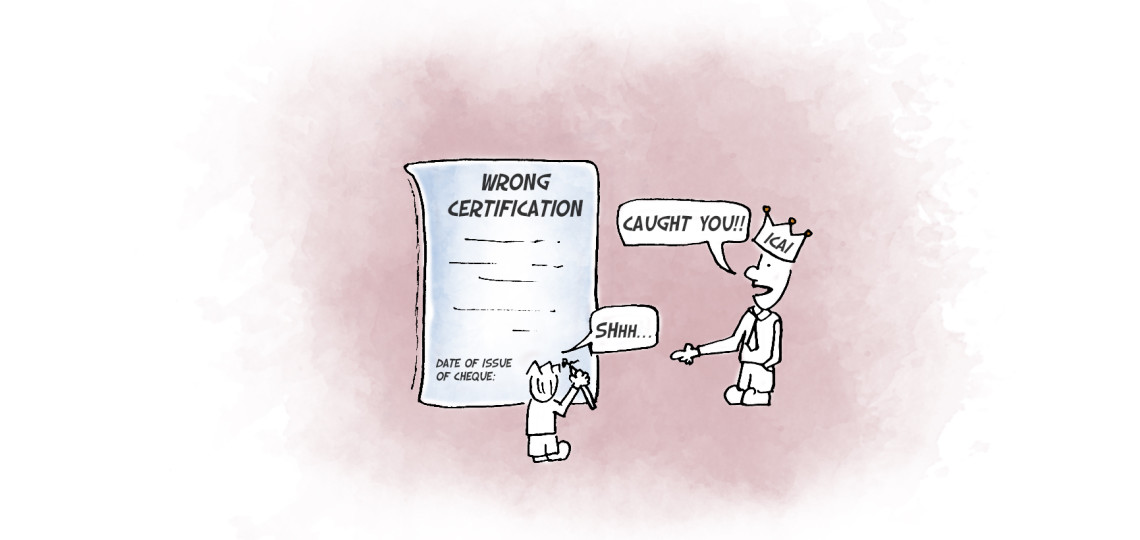

In February, 2017, the High Court of Delhi took cognizance of a report submitted by SEBI to the Council of the Institute of Chartered Accountants of India, on the incorrect certificate issued by a practicing Chartered Accountant with regard to allotment of share application money by a listed private company.

Crux of the case

In the said case – Council of the Institute of Chartered Accountants of India vs. Kailash Chander Agarwal & anr 1, the SEBI initially conducted a detailed investigation into the three certificates issued by the practicing professional. In the certificate in which the professional certified about the receipt and allotment of share application monies, it was observed that the date of encashment of cheque was not consciously recorded. It was established beyond doubt that the share application money was received after the issue of the certificate by the professional.

The stand taken by regulators

The SEBI came to the conclusion that the certificate issued by the professional was false and misleading. The SEBI concluded that the professional colluded with the management of the company in defrauding the investors. The matter was then referred to the ICAI which formed a disciplinary committee. After several hearings, committee also concurred with the SEBI investigation report. Finding the professional guilty of gross professional misconduct, the professional body recommended the removal of the name of the professional from the institute for a period of 5 years.

Sharp focus on professionals

The above case yet again puts the spotlight on the professional (conduct or) misconduct of professionals especially Lawyers, Chartered Accountants, Company Secretaries and or Cost Accountants.

A profession is a vocation requiring knowledge in a specialized area that requires high degree of consistency in service.

- The existence of a body of specialised knowledge or techniques;

- Formalised method of acquiring training and experience;

- Formation of professional and ethical codes for the guidance of conduct;

Professional misconduct is behaviour not confirming to the prevailing standards or laws, dishonest intention, dereliction of duty or management especially by persons entrusted or engaged to act on another’s behalf. It can be an act done wilfully with wrong intention by people engaged in (any) profession.

The definition of misconduct is a wide expression. It is not exhaustive and is only relative in nature. The misconduct has to be construed with reference to the subject matter and context in which the case arises.

Each of the professional bodies have their own statutes and disciplinary committees that decide on the existence and intensity of misconduct by the professional. Over the years almost all professional bodies especially of Advocates, CA’s, CS’s and CWA’s have ruled that the following will constitute professional misconduct:

- Wilful misrepresentation as professional;

- Solicitation of work by circulation of notices and or advertisements;

- Undercutting / underselling remuneration with the intention of edging out competition

- Engaging in any other business or occupation without informing or obtaining consent of the statutory professional body under which they are registered.

- Sharing confidential information of client

- Entering into any agreements / arrangement that will lead to conflict of interest

- Misfeasance

- Malfeasance

Not all conduct is misconduct

However, there have been quite a few instances in which the Courts have overruled the decisions taken by the disciplinary committees of the professional statutory bodies. On 16th February, 2017, the division bench of the Supreme Court set aside the decision of the disciplinary committee passed in the T A Kathiru Kunju Vs. Jacob Mathai 2. The bench held that negligence, unless gross, would not amount to professional misconduct. In such offence there must be an element of moral delinquency.

An error of judgement was also considered not to constitute an offence of professional misconduct, unless there was an element of wrongful intention present. Therefore “misconduct” acquires its connotation from the context, delinquency in its performance and its impact on the given task.

WELCOME MOVE BY THE CIC

In February this year, the Central information Commission (CIC) has directed the Bar Council of Delhi to report or publish cases of professional misconduct of advocates, proven or otherwise, in compliance with the Right to Information Act. This has been done to enable the public know the credibility of the counsels who represent them.

The direction given by the CIC is at present only for the Advocates. It is only a matter of time before the members of other professional bodies are brought under this ambit.

It is pertinent to note here that each of the professional bodies are governed by their own regulations, ethical codes and conduct.

The Chartered Accountants Act 1949; The Company Secretaries Act, 1980 and The Cost and Work accountants Act, 1959 (including their regulations and amendments) contain similar provisions relating to the professional (mis) conduct. The offences of professional misconduct have been clearly tabulated based on their level of intensity. While most cases attract either penalty or temporary suspension from membership, some grave cases of misconduct are decided by the Courts’ and permanent suspension from membership is pronounced.

The scenario in other countries

Like in India, all other countries that have CPAs, Chartered Secretaries and Lawyers have very clearly defined laws, ethics and codes of conduct laid down. Professionals in countries such as the UK, Singapore, Australia, Hong Kong, Canada, Malaysia, South Africa, Zimbabwe and Bangladesh abide by the code of conduct and penal provisions laid down by the Institute of Certified Public Accountants (ICPA) Institute of Chartered Secretaries & Administrators (ICSA).

Conclusion

Professionals such as Advocates, Chartered Accountants, Company Secretaries and or Cost Accountants are a class apart from other non-professionals. This is not only due to the specialised education, training, skill and experience they continuously obtain in the course of their work, but primarily due to the nobility and high morals that is associated with each such profession. Such professions should not be viewed only as business, trade or means of furthering monetary and other gains. It is a mirror reflecting the attitude, honesty, integrity and credibility of the professional rendering such services. It is these qualities that continues to maintain the thin but clear line between professional conduct and misconduct thereby reinforcing people’s faith in the rule of law.

He holds a Bachelor’s and Master’s Degree in Corporate Secretaryship and a Degree in Law. He is a Fellow member of the Institute of Company Secretaries of India and an Associate Member of the Corporate Governance Institute, UK and Ireland. He has also completed a program from ISB on ‘Value Creation through Mergers and Acquisitions.

He holds a Bachelor’s and Master’s Degree in Corporate Secretaryship and a Degree in Law. He is a Fellow member of the Institute of Company Secretaries of India and an Associate Member of the Corporate Governance Institute, UK and Ireland. He has also completed a program from ISB on ‘Value Creation through Mergers and Acquisitions. Mr P Muthusamy is an Indian Revenue Service (IRS) officer with an outstanding career of 30+ years of experience and expertise in all niche areas of Indirect Taxes covering a wide spectrum including GST, Customs, GATT Valuation, Central Excise and Foreign Trade.

Mr P Muthusamy is an Indian Revenue Service (IRS) officer with an outstanding career of 30+ years of experience and expertise in all niche areas of Indirect Taxes covering a wide spectrum including GST, Customs, GATT Valuation, Central Excise and Foreign Trade. During his judicial role, he heard and decided a large number of cases, including some of the most sensitive, complicated, and high-stake matters on insolvency and bankruptcy, including many cases on resolution plans, shareholder disputes and Schemes of Amalgamation, De-mergers, restructuring etc.,

During his judicial role, he heard and decided a large number of cases, including some of the most sensitive, complicated, and high-stake matters on insolvency and bankruptcy, including many cases on resolution plans, shareholder disputes and Schemes of Amalgamation, De-mergers, restructuring etc., A K Mylsamy is the Founder, Managing Partner and the anchor of the firm. He holds a Degree in law and a Degree in Literature. He is enrolled with the Bar Council of Tamil Nadu.

A K Mylsamy is the Founder, Managing Partner and the anchor of the firm. He holds a Degree in law and a Degree in Literature. He is enrolled with the Bar Council of Tamil Nadu. Mr. K Rajendran is a former Indian Revenue Service (IRS) officer with a distinguished service of 35 years in the Indirect Taxation Department with rich experience and expertise in the fields of Customs, Central Excise, Service Tax and GST. He possesses Master’s Degree in English literature. Prior to joining the Department, he served for the All India Radio, Coimbatore for a period of about 4 years.

Mr. K Rajendran is a former Indian Revenue Service (IRS) officer with a distinguished service of 35 years in the Indirect Taxation Department with rich experience and expertise in the fields of Customs, Central Excise, Service Tax and GST. He possesses Master’s Degree in English literature. Prior to joining the Department, he served for the All India Radio, Coimbatore for a period of about 4 years. An MBA from the Indian Institute of Management, Calcutta, and an M.Sc. in Tourism Management from the Scottish Hotel School, UK, Ashok Anantram was one fo the earliest IIM graduates to enter the Indian hospitality industry. He joined India Tourism Development Corporation (ITDC) in 1970 and after a brief stint proceeded to the UK on a scholarship. On his return to India, he joined ITC Hotels Limited in 1975. Over the 30 years in this Organisation, he held senior leadership positions in Sales & Marketing and was its Vice President – Sales & Marketing. He was closely involved in decision making at the corporate level and saw the chain grow from a single hotel in 1975 to a very large multi-brand professional hospitality group.

An MBA from the Indian Institute of Management, Calcutta, and an M.Sc. in Tourism Management from the Scottish Hotel School, UK, Ashok Anantram was one fo the earliest IIM graduates to enter the Indian hospitality industry. He joined India Tourism Development Corporation (ITDC) in 1970 and after a brief stint proceeded to the UK on a scholarship. On his return to India, he joined ITC Hotels Limited in 1975. Over the 30 years in this Organisation, he held senior leadership positions in Sales & Marketing and was its Vice President – Sales & Marketing. He was closely involved in decision making at the corporate level and saw the chain grow from a single hotel in 1975 to a very large multi-brand professional hospitality group. Mani holds a Bachelor Degree in Science and P.G. Diploma in Journalism and Public Relations. He has a rich and varied experience of over 4 decades in Banking, Finance, Hospitality and freelance Journalism. He began his career with Andhra Bank and had the benefit of several training programs in Banking.

Mani holds a Bachelor Degree in Science and P.G. Diploma in Journalism and Public Relations. He has a rich and varied experience of over 4 decades in Banking, Finance, Hospitality and freelance Journalism. He began his career with Andhra Bank and had the benefit of several training programs in Banking. Mr. Kailash Chandra Kala joined the Department of Revenue, Ministry of Finance as ‘Customs Appraiser’ at Mumbai in the year 1993.

Mr. Kailash Chandra Kala joined the Department of Revenue, Ministry of Finance as ‘Customs Appraiser’ at Mumbai in the year 1993.

S Ramanujam, is a Chartered Accountant with over 40 years of experience and specialization in areas of Corporate Tax, Mergers or Demergers, Restructuring and Acquisitions. He worked as the Executive Vice-President, Group Taxation of the UB Group, Bangalore.

S Ramanujam, is a Chartered Accountant with over 40 years of experience and specialization in areas of Corporate Tax, Mergers or Demergers, Restructuring and Acquisitions. He worked as the Executive Vice-President, Group Taxation of the UB Group, Bangalore. K K Balu holds a degree in B.A and B.L and is a Corporate Lawyer having over 50 years of Legal, Teaching and Judicial experience.

K K Balu holds a degree in B.A and B.L and is a Corporate Lawyer having over 50 years of Legal, Teaching and Judicial experience. Justice M. Jaichandren hails from an illustrious family of lawyers, academics and politicians. Justice Jaichandren majored in criminology and then qualified as a lawyer by securing a gold medal. He successfully practiced in the Madras High Court and appeared in several civil, criminal, consumer, labour, administrative and debt recovery tribunals. He held office as an Advocate for the Government (Writs Side) in Chennai and was on the panel of several government organizations as senior counsel. His true passion lay in practicing Constitutional laws with focus on writs in the Madras High Court. He was appointed Judge, High Court of Madras in December 2005 and retired in February 2017.

Justice M. Jaichandren hails from an illustrious family of lawyers, academics and politicians. Justice Jaichandren majored in criminology and then qualified as a lawyer by securing a gold medal. He successfully practiced in the Madras High Court and appeared in several civil, criminal, consumer, labour, administrative and debt recovery tribunals. He held office as an Advocate for the Government (Writs Side) in Chennai and was on the panel of several government organizations as senior counsel. His true passion lay in practicing Constitutional laws with focus on writs in the Madras High Court. He was appointed Judge, High Court of Madras in December 2005 and retired in February 2017. S Balasubramanian is a Commerce and Law Graduate. He is a member of the Delhi Bar Council, an associate Member of the Institute of Chartered Accountants of India, the Institute of Company Secretaries of India and Management Accountants of India.

S Balasubramanian is a Commerce and Law Graduate. He is a member of the Delhi Bar Council, an associate Member of the Institute of Chartered Accountants of India, the Institute of Company Secretaries of India and Management Accountants of India.